Build Your Business Budget

Spend smarter with a guided budgeting tool

Follow a step-by-step process to create an accurate business budget — even if you have no financial background.

As seen in:

Creating an accurate budget is tricky without any guidance

-

-

-

LivePlan walks you through the entire budgeting process

Get detailed guidance every step of the way

Not sure how to get started? Or what details to include? LivePlan gives you a step-by-step process for completing every aspect of your budget.

Build profit & loss statements, cash flow forecasts and more Read definitions of key terms and metrics Get AI-generated suggestions if you're not sure what to include

Using Xero or QuickBooks?

Build your budget five times faster than with spreadsheets by syncing your accounting data with LivePlan. You'll get a draft budget, based on historical data, that you can use as a starting point.

See how LivePlan works with:

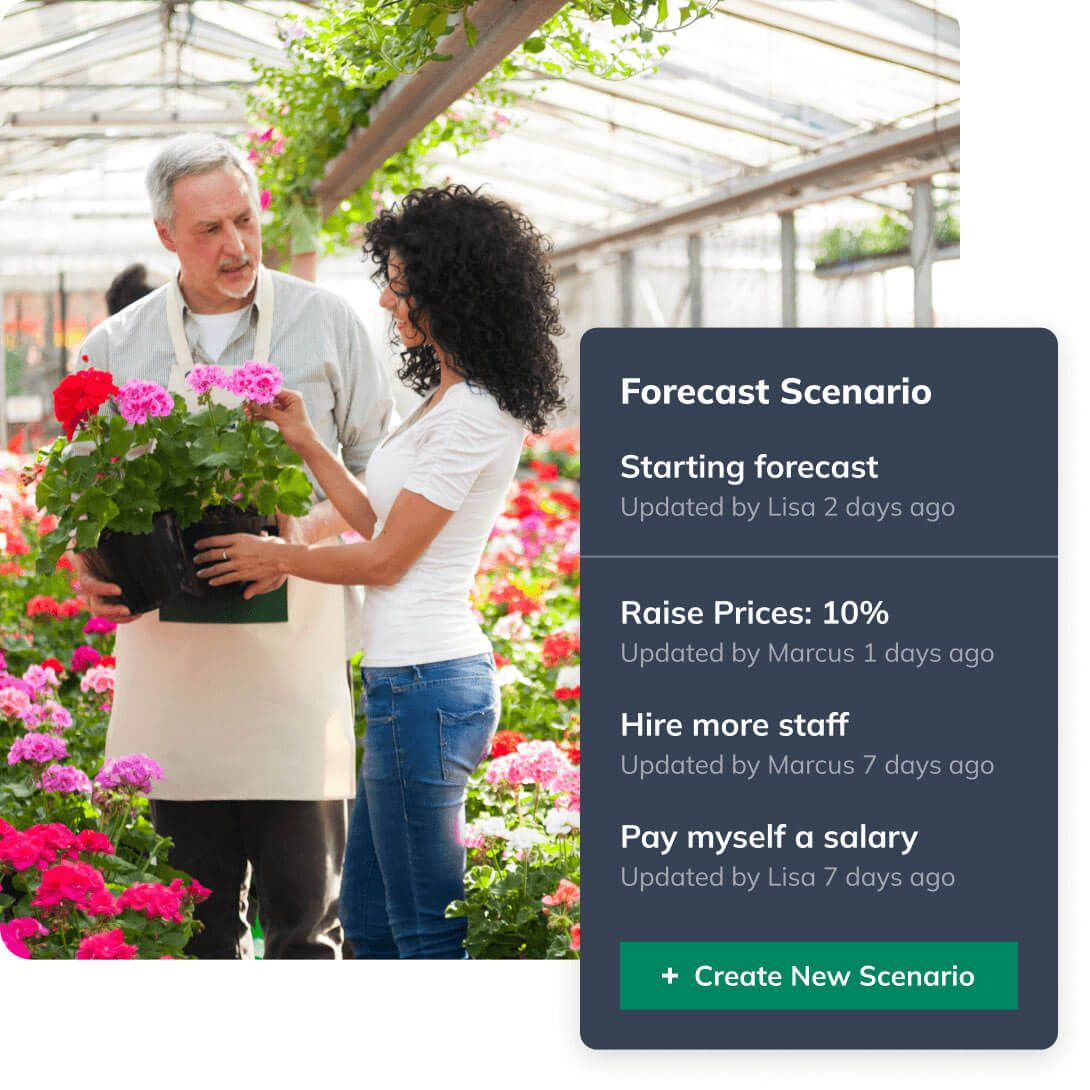

Build multiple budgets to test different scenarios

What if you hired more staff? Or spent more on inventory? Try out different spending scenarios to see how they impact your finances. You'll get five-year projections for profit and loss, cash at the end of the year and other metrics.

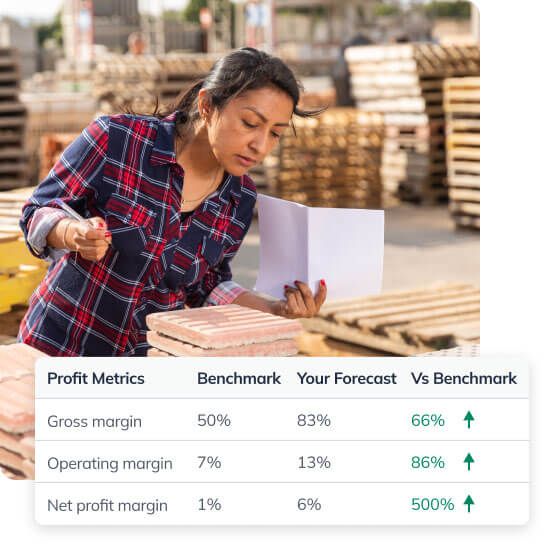

Budget smarter using industry benchmarks

Better understand how much you should be spending on marketing, rent and more with built-in industry benchmark data. It's a quick way to compare your budget to similarly sized businesses in your region.

Get benchmark data for 13 data points, including spending and profit metrics Compare your forecast and results to industry benchmarks at a glance Get data for specific regions and timeframes

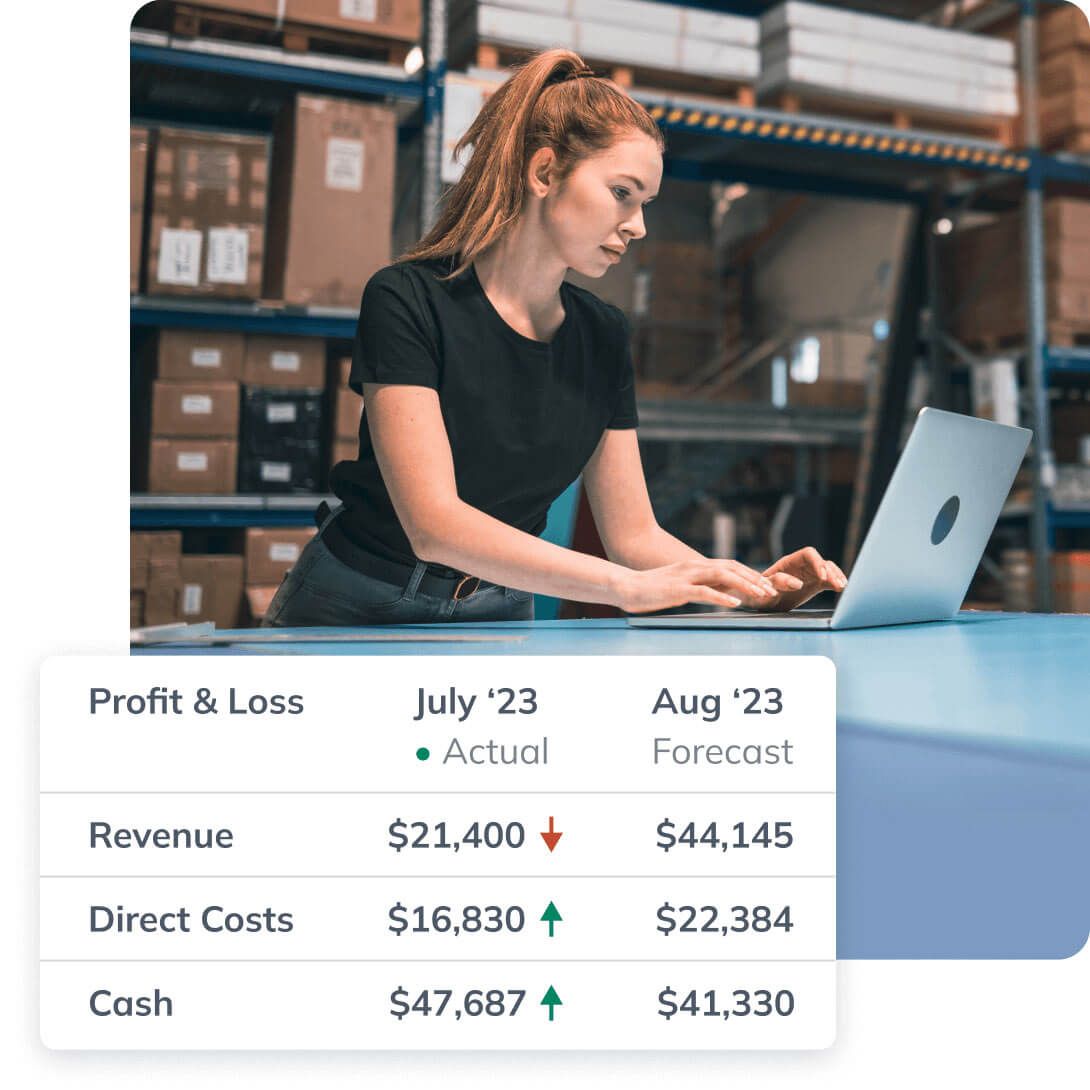

Reach your goals faster with performance tracking

Accountability is everything. Track your actual revenue and expenses against your budget to see if your business is headed in the right direction. That way, you can adjust your business strategy based on the data to maximize growth.

Sync Xero or QuickBooks to get real-time dashboards Spot opportunities to reduce expenses Set financials goals and understand what it will take to reach them

Plenty of support to help you succeed

Inspiration powered by AI

Instantly generate ideas at each step of your plan. You can also access 550+ sample plans to find one that matches your industry.

Guidance from business experts

Stay on track with video walk-throughs, webinars, and more from business planning experts.

If you ever get stuck, our team will help

If you ever have a question, you can instantly chat with a LivePlan expert.